This article was written by Hayden Flinn, Guo Sun Lee, Jingjing Jiang, Cindy Shek, Minny Siu and Justin Cherrington.

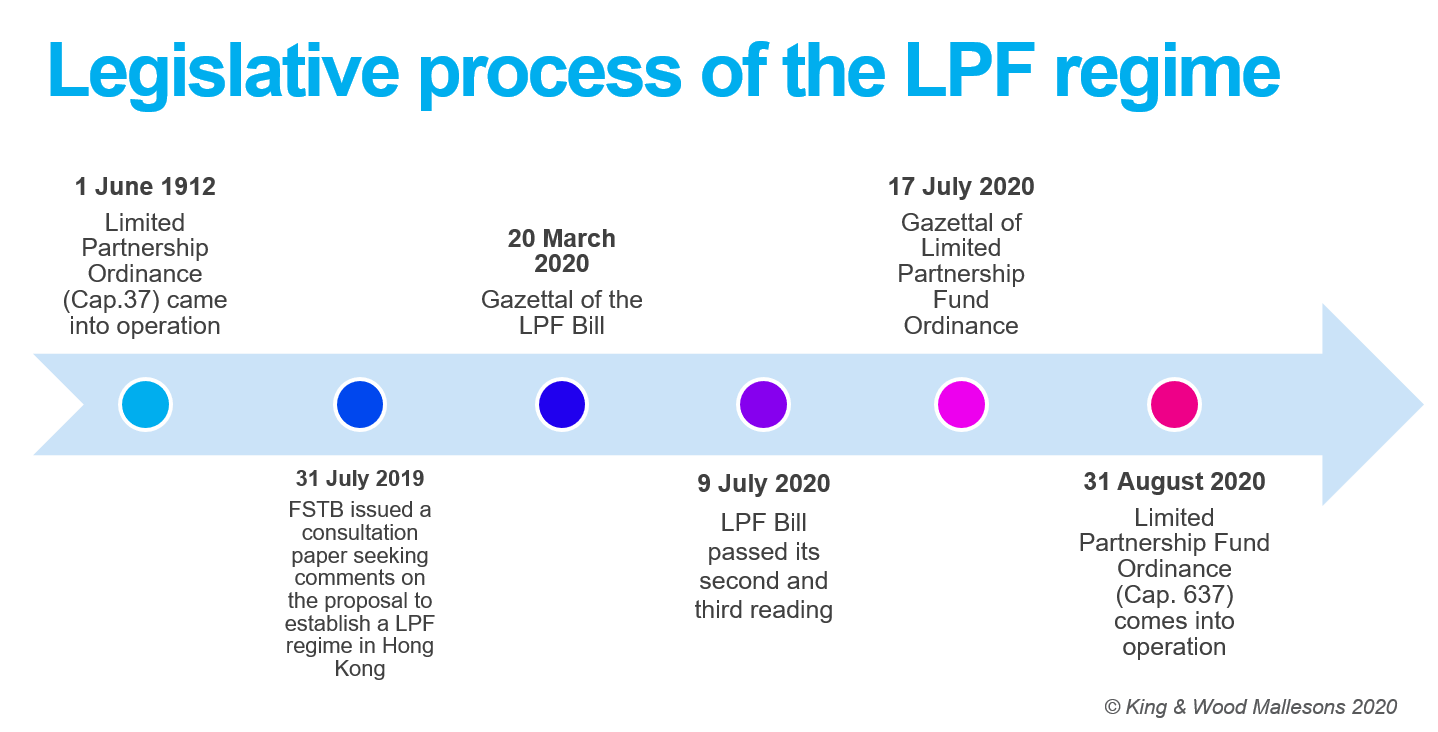

With the Legislative Council passing its second and third reading of the Limited Partnership Fund Bill ("Bill") on 9 July and gazettal of the Limited Partnership Fund Ordinance (Cap.637) ("LPFO") on 17 July, the long-awaited Hong Kong* Limited Partnership Fund ("LPF") regime is finally set to sail on 31 August 2020.

In addition to forming an open-ended fund company ("OFC") or a unit trust, the introduction of the LPF regime now provides fund managers with the option of setting up funds structured as a limited partnership in Hong Kong.

For the general framework and features of the Hong Kong LPF regime, please refer to our earlier publication (Is Hong Kong ready for its own limited partnership fund regime?).

This article identifies the key issues fund managers and sponsors should consider in light of the new LPF regime.

What has changed since March?

The Bill was scrutinised by the Legal Services Division since its introduction in March. Whilst remaining largely intact, several amendments were introduced. In particular, section 24(2)(c) of the Bill requires a statement by the General Partner ("GP") in the annual return as to whether the LPF will remain in operation, or will carry on business as a fund 12 months after the anniversary of the latest annual return submitted to the Companies Registrar ("Registrar"). Amendments to section 89 of the Bill has also been introduced to define the burden and standard of proof in respect of a person for a specified offence under the LPFO.

The GP and the investment manager

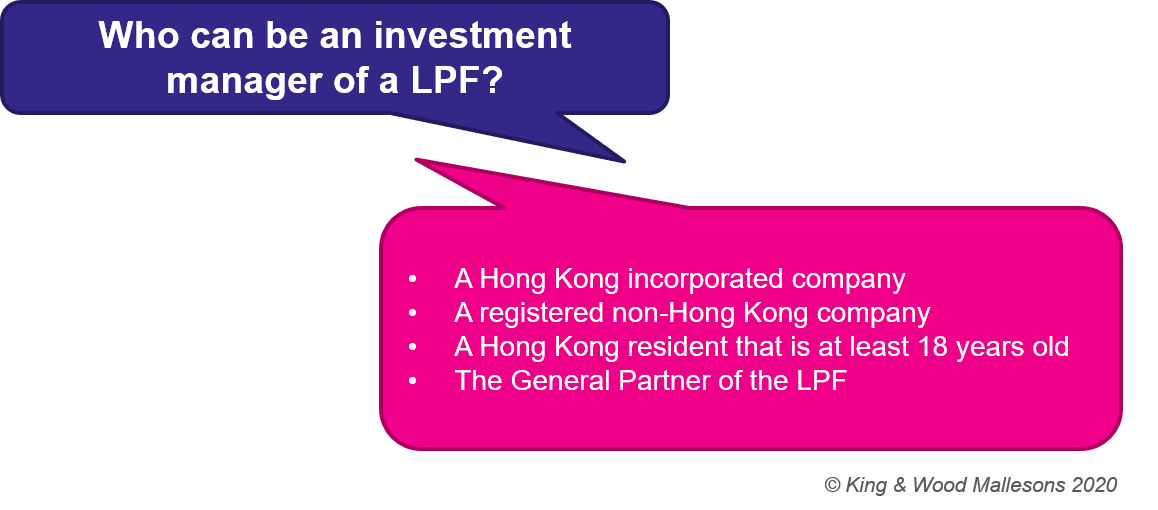

As noted in our earlier publication, the GP is required to appoint an investment manager to conduct day-to-day investment management functions.

Must the GP and/or the investment manager be licensed?

If the GP has fully delegated the investment management activities to the investment manager, the GP may not need to be licensed. In turn, unlike the Hong Kong OFC, the GP does not necessarily need to appoint an Securities and Futures Commission ("SFC") licensed entity to act as the investment manager if the LPF will not be carrying on a business of regulated activities in Hong Kong.

The SFC clarified the licensing requirements applicable to private equity funds earlier this year[1]. In summary, if a person conducts regulated activities in Hong Kong, he would need to be licensed irrespective of his role in the LPF (the likely roles which may trigger a licensing requirement include the GP, the investment manager, the investment committee, the distributor or placement agent). Unless otherwise exempted, licensing requirements may be triggered when a person or entity deals in, advises on or manages a portfolio of assets (this may include private equity and venture capital investments) which fall within the definition of "securities" under the SFO.

A GP or an investment manager of a LPF which does not invest in "securities" (e.g. the LPF invests in shares in a Hong Kong private company, non-securities assets such as real estate or other commodities) may be able to remain unlicensed. It should be noted that although shares or debentures of a Hong Kong private company falls outside the definition of "securities" under the SFO, shares or debentures of private companies incorporated outside of Hong Kong would still be considered as "securities".

Although retaining unlicensed GP and/or the investment manager may mean the LPF is free from the SFC's direct supervision hence arguably lowering regulatory and compliance costs, certain market players including investors and various service providers may prefer to deal with licensed sponsors so as to comply with their internal approval process and provide additional regulatory comfort. Fund managers may wish to plan ahead and consider if they wish to set up a fund management business in Hong Kong, or partner with licensed entities.

Do I need to appoint a custodian?

The GP is not required to appoint a third party custodian to demonstrate proper custody of the LPF assets under the LPFO. However, to the extent that the GP or the investment manager is a Type 9 licensee, the requirements under the SFC's Fund Manager Code of Conduct will apply to the investment management activities in respect of the LPF. This includes a requirement for the GP or the investment manager (as applicable) to: (a) exercise due skill, care and diligence in the appointment of the custodian; or (b) if self-custody is adopted, the GP or the investment manager must adopt policies and enforce procedures to separate custodial functions from its investment management functions.

Responsible person of the LPF and its obligations

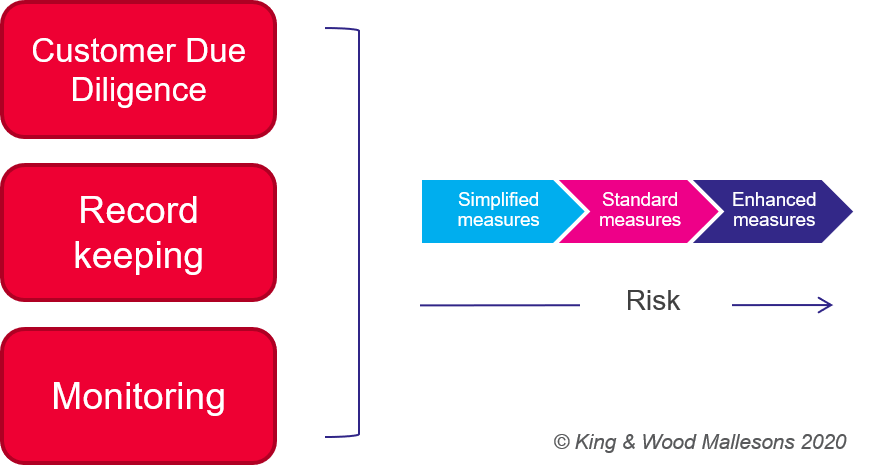

The LPFO requires a GP to appoint a responsible person ("RP") to conform with the Anti-Money Laundering ("AML") and Counter Terrorist Financing ("CTF") obligations of the LPF against each customer of the LPF (including the limited partners of the LPF) in accordance with Schedule 2 of the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (Cap.615) ("AMLO").

The RP will remain ultimately responsible for the LPF's AML/CTF obligations under the LPFO, which is notably different from other jurisdictions including Singapore and the Cayman Islands where the ultimate responsibility of AML/CTF compliance rests with the GP (although the GP can outsource such functions to third party service providers).

Below shows an overview of the requirements under Schedule 2 of the AMLO:

Given the LPFO requires the RP to be an authorised institution, a licensed corporation, an accounting professional or a legal professional, such parties are already subject to the AMLO. Implementation of AML/CTF measures should therefore be relatively straightforward. For instance, a LPF managed by a Type 9 licensee should be able to leverage its existing AML/CTF policies and measures that are already in place when managing an offshore domiciled limited partnership fund.

As the global financial services sector is steering towards digitisation of their services and processes, the regulators have also caught up by updating the Hong Kong Monetary Authority AML Guidelines and SFC Guideline on Anti-Money Laundering and Counter-Terrorist Financing in late 2018, which provide guidance to authorised institutions and licensed entities on remote customer onboarding from the AML and ongoing compliance perspectives. Accordingly, LPFs may thereby onboard investors by utilising these remote measures. Please refer to our earlier publications on virtual client onboarding by financial institutions and licensed corporations.

Registration and ongoing compliance

The LPF regime adopts an opt-in registration scheme which does not require SFC authorisation or approval unless the LPF is targeted to the retail public.

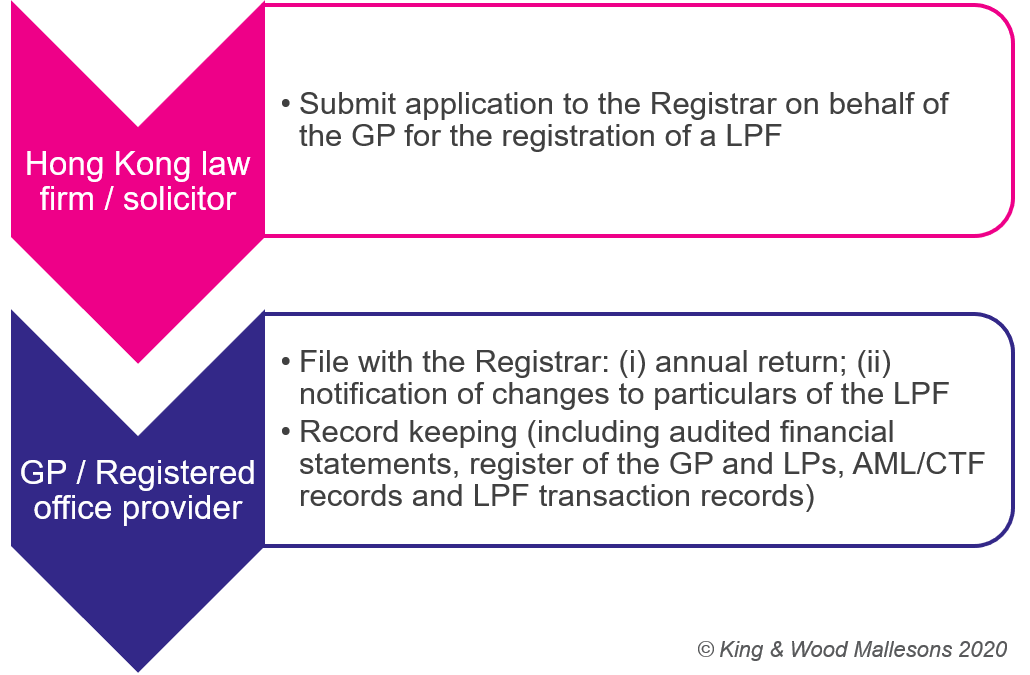

The LPF application pack is to be submitted by a Hong Kong law firm or a solicitor. Similar to a private company in Hong Kong, the LPF is required to file annual returns and notify the Registrar for change of particulars. Schedule 3 of the LPFO also prescribes fees for lodging a registration application, filing annual return and notification of change, which are all notably lower than the existing fees charged by our Cayman counterpart.

It is advisable for fund sponsors to start lining up their service providers, including the administrator or company secretarial providers[2], who may assist with these ongoing regulatory obligations.

Tax implications

As with any fund jurisdictions, tax treatment continues to play a vital role in fund structuring. With the recent publication of the interpretation and practice notes in respect of profits tax exemption for funds by the Inland Revenue Department (referred as DIPN 61), there is now further clarity as to the taxation of each fund entity (including the relevant LPFs and any special purpose entities), investor and the investment manager in terms of whether they qualify for the unified fund tax exemption ("UFE").

Taxation implications for the LPF and special purpose entity

The UFE was contained in the Inland Revenue (Profits Tax Exemption for Funds) (Amendment) Ordinance 2019 which came into effect on 1 April 2019. The UFE provides a jurisdictionally neutral tax treatment for private funds in Hong Kong. In summary, private funds (including LPFs) will be exempted from profits tax in Hong Kong as long as they meet the definition of a "fund" and satisfy certain conditions. To qualify for the UFE, the relevant profits of the LPF must derive from "qualifying transactions" (including transactions in securities, futures contracts, shares in private companies and foreign currencies etc) that are carried out or arranged in Hong Kong by an authorised institution or licensed corporation or where the LPF is a qualified investment fund. This profit tax exemption, subject to certain conditions, also applies to special purpose entities held by the LPF.

Further, unlike Singapore which requires the GP to apply to the local monetary authority for tax exemption, the UFE does not impose pre-approval requirements. Rather it allows for self-assessment by the relevant entity to determine if the LPF satisfies the relevant conditions to be profit tax exempt.

The subscription, transfer or redemption of LPF interest will not attract Hong Kong stamp duty as it does not fall under the definition of "stock". However, stamp duty will apply where the LPF accepts capital contributions or distributes profits in kind which involve the transfer of dutiable assets (such as Hong Kong stock or immovable property).

Taxation implications for the investment manager/investment advisor

Management fee received by a Hong Kong-based investment manager will generally be subject to profits tax of 16.5% without specific tax incentive. However, as Hong Kong adopts a territorial concept of taxation, only profits sourced in Hong Kong would be subject to Hong Kong taxation. Hence, if the core investment management activities are conducted outside of Hong Kong, an offshore claim on the relevant portion of the management fee income can be applied for to lower the profits tax. This may be relevant and favourable to investment managers with transnational presence.

Carried interest remains unresolved

The Financial Secretary announced earlier this year in the Budget that the Hong Kong Government aims to provide more certainty on carried interest taxation which has yet been clarified. The industry is expecting attractive tax concession on carried interest to complement the LPF regime and completing the Hong Kong investment management ecosystem.

Fund documentation

The LPFO affirms contractual freedom among partners of a LPF[3], which is on par with many other popular offshore fund jurisdictions. Accordingly, there should be no need for a complete overhaul of the existing fund documentation that fund sponsors and investors have been using for existing funds established in other jurisdictions.

There is no requirement for a LPF to have a private placement memorandum or an offering document, and the GP is not required to file the same with the Registrar or the SFC. This is contrary to the Cayman regime which, under the revised Private Funds Law, 2020, requires either a private placement memorandum, a summary of terms or marketing materials containing certain prescribed information to be filed with the Cayman Islands Monetary Authority.

Fund sponsors who are looking to conduct fundraising with the LPF structure may wish to start revisiting existing fund documents with their legal advisers to cater for jurisdiction-specific amendments.

The way forward

The LPFO does not currently allow re-domiciliation of offshore funds to become an LPF in Hong Kong. We look forward to the Hong Kong Government introducing such mechanism as an enhancement to the LPF regime as we understand a lot of market players are exploring this possibility.

The LPF regime is undoubtedly introduced at an opportune time. With the recent changes to Cayman private funds regulations, ranging from more stringent reporting and filing obligations and economic substance requirements to changes in legislations, the initial attractiveness derived from tax benefits and reporting laxity has largely subsided. We also see a global trend where fund sponsors are preferring to align the substance of asset management activities with the fund domicile. In addition, Hong Kong's proximity to Mainland China and its membership in the Greater Bay Area forms a breeding ground for attractive investment opportunities in fast-growing industries ranging from technology, media and telecom, healthcare, biomedical to fintech companies.

King & Wood Mallesons has a dedicated team across our network focusing on fund formation, regulatory, licensing and taxation advice. We look forward to working with our clients on these exciting initiatives. Please speak to us if you have any questions.

The authors would like to thank Florence Lau and Boer Ma for their contributions to this article.

*Any reference to "Hong Kong" or "Hong Kong SAR" shall be construed as a reference to "Hong Kong Special Administrative Region of the People's Republic of China".

[1] SFC's circular dated 7 January 2020 entitled "Circular to private equity firms to be licensed", accessible at: https://www.sfc.hk/edistributionWeb/gateway/EN/circular/doc?refNo=20EC2

[2] King & Wood Mallesons has a dedicated corporate advisory and company secretarial team which can assist you with preparing and arranging ongoing filings with the Registrar and provide registered office facility to the LPF. Please contact us if you wish to obtain further information.

[3] Section 16(1) of the LPFO.